Understanding cash vs accrual accounting is one of the most important decisions you’ll make as a business owner. It’s not just about bookkeeping—it directly affects your profits, taxes, financial clarity, and long-term growth.

Many businesses start simple, but as operations expand, the limitations of the wrong accounting method become clear. Choosing the right one early can save you from costly adjustments later.

Key Takeaways

- Cash accounting tracks real-time money flow

- Accrual accounting reflects true financial performance

- Your choice impacts taxes, reporting, and decisions

- Compliance rules may require accrual accounting

- The right method depends on your business goals

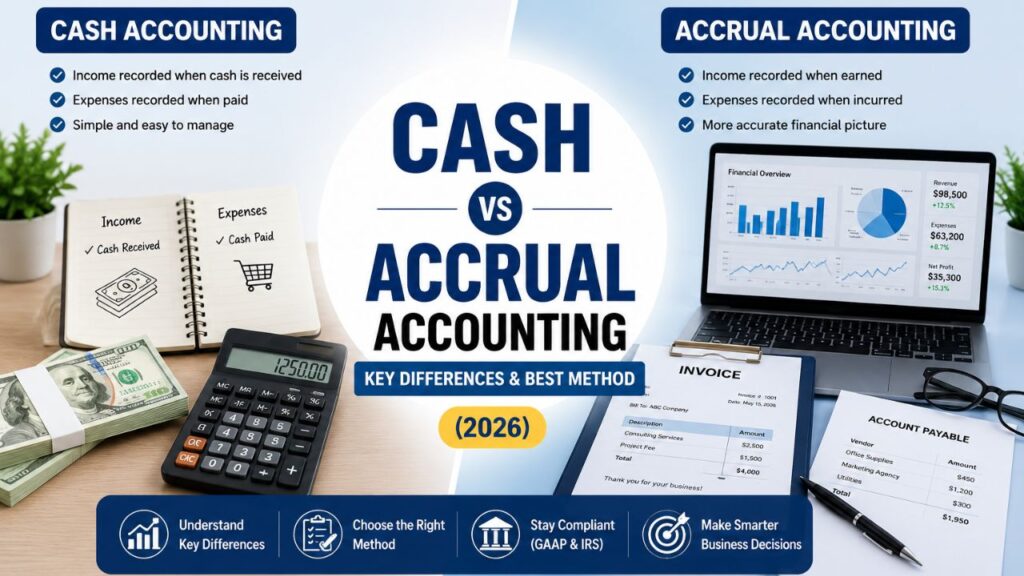

What is Cash Accounting?

Cash accounting records transactions only when cash actually moves—when you receive money or pay expenses.

Example

If you send an invoice in January and get paid in March, the income is recorded in March.

Best For

- Freelancers

- Small businesses

- Low-volume operations

Advantages

- Simple and easy to manage

- Clear cash flow visibility

- Minimal accounting effort

Limitations

- Doesn’t reflect future obligations

- Can distort profitability

- Not ideal for scaling businesses

What is Accrual Accounting?

Accrual accounting records transactions when they are earned or incurred, regardless of cash movement.

Example

If you send an invoice in January, it’s recorded in January—even if payment arrives later.

Best For

- Growing businesses

- eCommerce stores

- Companies handling inventory

Advantages

- Accurate financial reporting

- Matches revenue with expenses

- Better for planning and forecasting

Limitations

- More complex to manage

- Requires proper systems

- Cash flow not immediately visible

Cash vs Accrual Accounting: Key Differences

| Feature | Cash Accounting | Accrual Accounting |

| Revenue | When received | When earned |

| Expenses | When paid | When incurred |

| Complexity | Low | High |

| Accuracy | Limited | High |

| Taxation | Based on cash | Based on earned income |

| Suitability | Small businesses | Growing businesses |

GAAP Compliance and IRS Requirements

When choosing between cash vs accrual accounting, compliance plays a critical role—especially under Generally Accepted Accounting Principles (GAAP) and the Internal Revenue Service.

GAAP Compliance

- GAAP typically requires accrual accounting

- Financial statements must reflect true performance

- Revenue and expenses must align within the same period

This makes accrual accounting essential for businesses seeking investors or professional reporting.

IRS Requirements

- Small businesses may use cash accounting

- Businesses with inventory or higher revenue often must use accrual

- Changing methods requires IRS approval

In short:

- Cash = flexibility

- Accrual = compliance + scalability

How to Choose the Right Accounting Method for Your Business

Selecting between cash vs accrual accounting depends on your business structure, goals, and growth plans.

1. Business Size

- Small → Cash accounting

- Growing → Accrual accounting

2. Cash Flow Needs

- Need real-time cash tracking → Cash

- Need full financial insight → Accrual

3. Inventory Handling

If your business deals with inventory, accrual accounting is usually required.

4. Growth Plans

Planning to scale or attract investors? Accrual accounting is the better choice.

5. Tax Strategy

- Cash accounting delays taxes until payment is received

- Accrual accounting may require earlier tax payments

Tax Implications You Should Know

Your accounting method directly impacts how and when you pay taxes:

- Cash Accounting: Taxed on received income

- Accrual Accounting: Taxed on earned income

This difference can significantly affect your cash flow and financial planning.

Common Mistakes to Avoid

- Using cash accounting for a growing eCommerce business

- Ignoring unpaid invoices

- Mixing both accounting methods incorrectly

- Delaying the switch to accrual accounting

Why Most Businesses Eventually Switch to Accrual

As businesses grow, accrual accounting becomes necessary because it:

- Provides a complete financial picture

- Improves decision-making

- Supports investor requirements

- Aligns with global standards

This is why most successful businesses transition from cash to accrual accounting over time.

PlugBooks Recommendation for Sellers

If you’re selling on platforms like Amazon or eBay, choosing the right method in cash vs accrual accounting is crucial.

PlugBooks helps you:

- Automate your bookkeeping

- Integrate with QuickBooks & Xero

- Track real profits, not just cash flow

- Stay compliant with tax regulations

Whether you’re starting or scaling, the right tools combined with the right accounting method can transform your business finances.

FAQs

1. What is the main difference between cash vs accrual accounting?

Cash accounting records transactions when money moves, while accrual records them when they occur.

2. Which accounting method is better for small businesses?

Cash accounting is simpler, but accrual accounting is better for growth.

3. Can I switch from cash to accrual accounting later?

Yes, most businesses switch as they expand.

4. Is accrual accounting required by law?

It is often required for larger businesses or those with inventory.

5. Does cash accounting affect taxes?

Yes, taxes are based on received income in cash accounting.

6. Why do investors prefer accrual accounting?

Because it provides a more accurate financial picture.

7. Do banks prefer accrual or cash basis accounting?

Most banks prefer accrual accounting because it shows a complete view of financial health, including receivables and liabilities, which helps in loan decisions.

Quick Recap

- Cash accounting = simple, cash-based tracking

- Accrual accounting = accurate, growth-focused reporting

- Compliance often favors accrual accounting

- Your business stage determines the right method

Conclusion

Choosing between cash vs accrual accounting is more than a technical decision—it’s a strategic one.

If simplicity and immediate cash tracking are your priority, cash accounting works. But if your goal is growth, accuracy, and long-term success, accrual accounting is the better path.

The smartest approach is to align your accounting method with where your business is today—and where you want it to be tomorrow.